All you need to know about

Medigap Plans

A Medicare Supplement Insurance (Medigap) policy is health insurance that can help pay some of the health care costs that Original Medicare doesn’t cover, like coinsurance, copayments, or deductibles. Private insurance companies sell Medigap policies. Some Medigap policies also cover certain benefits Original Medicare doesn’t cover, like emergency foreign travel expenses. Medigap policies don’t cover your share of the costs under other types of health coverage, including Medicare Advantage Plans (like HMOs or PPOs), standalone. Medicare Prescription Drug Plans, employer/union group health coverage, Medicaid, or TRICARE. Insurance companies generally can’t sell you a Medigap policy if you have coverage through Medicaid or a Medicare Advantage Plan. Contact Mark Turner Insurance in Staten Island to find out if a Medigap policy is right for you.

When’s the best time to buy a Medigap policy?

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This period lasts for 6 months and begins on the first day of the month in which you’re both 65 or older and enrolled in Medicare Part B. Some states (like NY) have additional Open Enrollment Periods including those for people under 65. During this period, an insurance company can’t use medical underwriting to decide whether to accept your application. This means the insurance company can’t do any of these because of your health problems:

- Refuse to sell you any Medigap policy it offers.

- Charge you more for a Medigap policy than they charge someone with no health problems.

- Make you wait for coverage to start (except as explained below).

While the insurance company can’t make you wait for your coverage to start, it may be able to make you wait for coverage related to a pre-existing condition. A pre-existing condition is a health problem you have before the date a new insurance policy starts. In some cases, the Medigap insurance company can refuse to cover your out-of-pocket costs for these pre-existing health problems for up to 6 months. This is called a “pre-existing condition waiting period.” After 6 months, the Medigap policy will cover the pre-existing condition. Coverage for a pre-existing condition can only be excluded if the condition was treated or diagnosed within 6 months before the coverage starts under the Medigap policy. This is called the “look-back period.” Remember, for Medicare‑covered services, Original Medicare will still cover the condition, even if the Medigap policy won’t, but you’re responsible for the Medicare coinsurance or copayment.

Why is it important to buy a Medigap policy when I’m first eligible?

When you’re first eligible, you have the right to buy any Medigap policy offered in your state. In addition, you generally will get better prices and more choices among policies. It’s very important to understand your Medigap Open Enrollment Period. Outside of Medigap Open Enrollment, Medigap insurance companies are generally allowed to use medical underwriting to decide whether to accept your application and how much to charge you for the Medigap policy. However, if you apply during your Medigap Open Enrollment Period, you can buy any Medigap policy the company sells, even if you have health problems, for the same price as people with good health. If you apply for Medigap coverage after your Open Enrollment Period, there’s no guarantee that an insurance company will sell you a Medigap policy if you don’t meet the medical underwriting requirements.

It’s also important to understand that your Medigap rights may depend on when you choose to enroll in Medicare Part B. If you’re 65 or older, your Medigap Open Enrollment Period begins when you enroll in Part B, and it can’t be changed or repeated. After your Medigap Open Enrollment Period ends, you may be denied a Medigap policy or charged more for a Medigap policy due to past or present health problems. In most cases, it makes sense to enroll in Part B and buy a Medigap policy when you’re first eligible for Medicare, because you might otherwise have to pay a Part B late enrollment penalty and might miss your 6-month Medigap Open Enrollment Period. However, there are exceptions if you have employer coverage. If you have any questions about your Medigap policy eligibility in Staten Island, contact our Medicare insurance agency.

What Medigap Policies Cover?

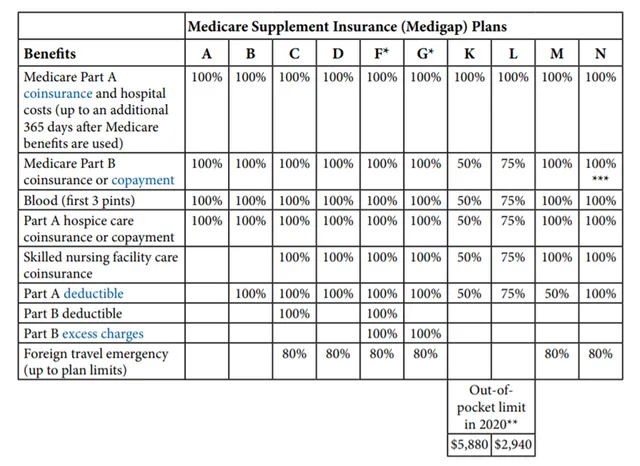

Plans available.

You’ll need more details than this chart provides to compare and choose a policy.

- Insurance companies selling Medigap policies are required to make Plan A available. If they offer any other Medigap policy, they must also offer either Plan C or Plan F to individuals who are not new to Medicare and either Plan D or Plan G to individuals who are new to Medicare.

- Plans D and G with coverage starting on or after June 1, 2010, have different benefits than Plans D or G bought before June 1, 2010.

- Plans E, H, I, and J are no longer sold, but, if you already have one, you can generally keep it.

- Starting January 1, 2020, Medigap plans sold to people new to Medicare won’t be allowed to cover the Part B deductible. Because of this, Plans C and F will no longer be available to people who are new to Medicare on or after January 1, 2020.

– If you already have either of these two plans (or the high deductible version of Plan F) or are covered by one of these plans prior to January 1, 2020, you’ll be able to keep your plan. If you were eligible for Medicare before January 1, 2020 but not yet enrolled, you may be able to buy one of these plans.

– People new to Medicare are those who turn 65 on or after January 1, 2020, and those who get Medicare Part A (Hospital Insurance) on or after January 1, 2020.

The Chart Below Gives You a Quick Look at the Standardized Medigap:

* Plans F and G also offer a high-deductible plan in some states. With this option, you must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,340 in 2020 before your policy pays anything. (Plans C and F won’t be available to people who are newly eligible for Medicare on or after January 1, 2020.).

* Plans F and G also offer a high-deductible plan in some states. With this option, you must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,340 in 2020 before your policy pays anything. (Plans C and F won’t be available to people who are newly eligible for Medicare on or after January 1, 2020.).

** For Plans K and L, after you meet your out-of-pocket yearly limit and your yearly Part B deductible ($198 in 2020), the Medigap plan pays 100% of covered services for the rest of the calendar year.

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

What Medigap Policies Don’t Cover

- Medicare Advantage Plans (also known as Part C), like an HMO or PPO

- Medicare Prescription Drug Plans (Part D)

- Medicaid

- Employer or union plans, including the Federal Employees Health Benefits Program (FEHBP)

- TRICARE

- Veterans’ benefits

- Long-term care insurance policies

- Indian Health Service, Tribal, and Urban Indian Health plans

- Qualified Health Plans sold in the Health Insurance Marketplace

What types of Medigap policies can insurance companies sell?

In most cases, Medigap insurance companies can sell you only a “standardized” Medigap policy. All Medigap policies must have specific benefits, so you can compare them easily. If you live in Massachusetts, Minnesota, or Wisconsin.

Insurance companies that sell Medigap policies don’t have to offer every Medigap plan. However, they must offer Plan A if they offer any Medigap policy.

If they offer any plan in addition to Plan A, they must also offer Plan C or Plan F. Each insurance company decides which Medigap plan it wants to sell, although state laws might affect which ones they offer.

In some cases, an insurance company must sell you a Medigap policy if you want one, even if you have health problems.

Here are certain times that you’re guaranteed the right to buy a Medigap policy:

- When you’re in your Medigap Open Enrollment Period.

- If you have a guaranteed issue right.

You may be able to buy a Medigap policy at other times, but the insurance company can deny you a Medigap policy based on your health. Also, in some cases it may be illegal for the insurance company to sell you a Medigap policy (like if you already have Medicaid or a Medicare Advantage Plan). Contact Mark Turner Insurance today if you are interested in buying a Medigap policy in Staten Island.

Send Us A Message

Get a Free Quote

We’re Waiting To Help You

Medicare is complicated. We can help make it easy for you to understand and feel confident with your choices.